How to republish

Read the original article and consult terms of republication.

CVAE, Industrial Territories: the contradictions of French reindustrialisation policy

By Nadine Levratto, Head of Research at CNRS, Université Paris Nanterre – Université Paris Lumières, Luc Tessier, Associate Professor, EM Normandie, Philippe Poinsot, Assistant Professor, Université Gustave Eiffel.

Photo credits: Epictura - lagereek 55970755

Abolition of Company Value Added Tax (CVAE) contributions, creation of Industrial Territories… an increasing number of initiatives are being rolled out to accelerate reindustrialisation. But how exactly is this being done? And what if these initiatives were in fact contradictory, not complementary, therefore calling into question the overall vision and effectiveness of reindustrialisation efforts?

After decades of declining employment and the near indifference of industrial organisations, saving industry has become a national priority in France. Emphasis is put on the strategic nature of this sector, the associated issues of sovereignty, and the employment and regional dynamics that could result from a recovery or at least a halt in industry’s decline. Among the measures recently adopted with the goal of industrial reconquest in mind, two deserve a closer look, both because of their prominence in political discourse, and due to their respective specificities.

The gradual abolition of CVAE (company value added tax) represents a further reduction in "production tax" contributions collected by the organisations representing businesses. This measure is one of the standard tools of a supply-side policy aimed at increasing the competitiveness of companies, particularly industrial firms, by reducing their tax burden.

The "Industrial Territories" initiative (TI) is a national support programme for industrial development in specific geographical areas. This scheme is focused on developing local projects and partnerships between public and private stakeholders with the aim of revitalising areas where industry is considered to be a driver of economic development. This approach reflects the industrial policy rooted in these territories that relies on tangible and intangible local resources.

Two schemes, unbalanced cost

Another major difference between these two policies lies in their cost for the State budget. The abolition of CVAE will lead to a shortfall of 10 billion euros per year on a full-year basis, and means that the French government will need to allocate an equivalent sum of VAT to local authorities.

Budgetary expenditure for the new phase of the TI initiative is difficult to calculate given the reallocation of pre-existing programmes. For phase 1, no specific resources were allocated to the scheme, but the aim was to prioritise interventions by the State and its operators. For phase 2 (2023-2026), the allocated budget is around 200 million euros. The budgetary impact of each measure is therefore significantly different. In a recent article, we sought to characterise the profiles of territories and companies having benefited from the abolition of CVAE, and then to highlight the consistency of this measure with the TI initiative.

Mixed outcomes to be expected from the abolition of CVAE for industry

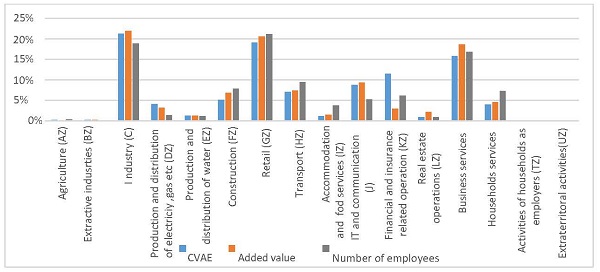

As we may have feared, the profile of CVAE contributors (Fig. 1) means that the abolition of this local tax contribution is not expected to have a massive, or even significant, impact on industrial companies. Although large and intermediate-sized industrial companies appear to be the main beneficiaries, with a share of 9.2% and 8.8% respectively of CVAE paid in 2020, large companies in the finance sector come in close behind them, with a share of 8.7%. We also note that all companies in the retail industry, from SMEs to large companies, benefit from this measure to a greater extent than the others, accounting for 18.7% of the amount of CVAE (7.1% for intermediate-sized companies, 6.8% for large companies and 4.8% for SMEs).

Share of each sector in 2020 in CVAE, added value and number of employees of companies contributing to CVAE

DGFiP, FLORES, FARE; Calculations from the authors, Provided by the author

DGFiP, FLORES, FARE; Calculations from the authors, Provided by the authorWe therefore come to the conclusion that the abolition of CVAE certainly has a positive effect on the industrial sector, by reducing the amount of income tax for companies subject to this contribution. However, it is not without its shortcomings. On the one hand, it is accompanied by a threshold effect, with SMEs and micro-enterprises only marginally affected by the reform. Secondly, it generates a significant deadweight effect, at least for the retail and ‘finance and insurance’ sectors. This distribution of gains by sector also raises questions about the effects of the reform on export price competitiveness and job creation in France. Indeed, these two sectors are either non-exporting (retail), or tend to set up subsidiaries abroad to reach foreign markets (finance and insurance).

A beneficial measure for the survival of companies in difficulty

A more detailed analysis of the impact of the measure according to the financial soundness of companies shows that industrial companies in a rather deteriorated financial state will benefit most from the abolition of CVAE. At first glance, this effect may be seen as positive: by improving the financial health of companies in difficulty, this reform means that companies which would otherwise have been likely to exit the market will remain there. However, this boost to fragile companies could prove temporary, as it is linked solely to a tax contribution and not to a better adaptation of a company’s internal organisation to their environment. This conclusion suggests that industrial policies should be dissociated from a general reduction in taxation.

Furthermore, an analysis of industrial companies according to their investment profile (Fig. 2) shows that the main beneficiaries are also those who already invest the most: 40% of investment is made by 1% of CVAE contributors, and 80% of investment is made by 10% of contributors. This concentration is particularly noticeable in transport equipment manufacturing, pharmaceuticals, coking and refining, as well as IT and electronic equipment manufacturing. Without having to make CVAE contributions, these companies could therefore invest more. But the effects are likely to be modest at best, since this tax contribution does not appear to have prevented them from investing.

Share of CVAE paid in industry for each type of investment from industrial companies subject to CVAE in 2020

Weak synergies between the abolition of CVAE and Industrial Territories

The analysis highlights a certain mismatch between the abolition of CVAE and the Industrial Territory policy, since it is not the same local authorities mainly affected by these measures. Indeed, it appears that there is only a slight overlap between the geographical areas that benefit most from the abolition of CVAE and those covered by the Industrial Territory policy. Only a third of CVAE is paid by companies located in Industrial Territory zones, and the abolition of this tax contribution does not directly encourage industrial development in these zones, since it is in fact ‘service-residential’ sectors, which are not especially industry-oriented, that contribute most to CVAE in Industrial Territory zones.

The abolition of CVAE could even have adverse effects on reindustrialisation and regional development, as it results in a significant loss of tax resources for the State, which could have used these funds to finance infrastructure or public services that are crucial to industrial development. Replacing a local tax with a VAT payout also represents a recentralisation of local authority financing and a further erosion of their fiscal autonomy, reducing their ability to respond to the specific needs of their territories. There is therefore a risk of widening the gap between local economic activity and the resources available to local authorities to support industrial development.

A change of policy?

As it currently stands, the decision to abolish CVAE, taken without prior in-depth analysis, would appear to be poorly targeted and poorly coordinated with Industrial Territory policy. As it will benefit all sectors and regions, regardless of order of priority, its impact on the reindustrialisation of France is likely to remain limited. At a time when public debt is a concern for the government and lawmakers, it seems imperative to abandon widespread tax relief. From now on, tax relief should be conditional on sectoral or regional criteria, in order to maximise the impact on reindustrialisation.

Ensuring a better match between local economic activity and local authority resources also seems necessary in order to guarantee a fair distribution of tax resources, taking into account the needs of local authorities and the impact on taxpayers, particularly businesses. Finally, it is essential to enhance the coherence of industrial policies by promoting complementary features between the various instruments adopted, and to better target priority areas and sectors. The country's industrial recovery depends more on the development of an all-round industrial policy than on the multiplication of costly and unfortunately ineffective measures, particularly tax cuts.

Identity card of the article

Original title: | CVAE, Territoires d’industrie : les contradictions de la politique de réindustrialisation à la française |

Author: | Nadine Levratto, Luc Tessier, Philippe Poinsot |

Publisher: | The Conversation France |

Collection: | The Conversation France |

Licence: | This article is republished from The Conversation France under Creative Commons licence. Read the original article. An English version was created by Hancock & Hutton for Université Gustave Eiffel and was published by Reflexscience under the same license. |

Date: | February 12, 2025 |

Languages: | French and English |

Key words: | companies, industry, economy, taxation, reindustrialisation |

![[Translate to English:] Licence creative commons BY-SA 4.0](https://reflexscience.univ-gustave-eiffel.fr/fileadmin/ReflexScience/Accueil/Logos/CCbySA.png "[Translate to English:] Licence creative commons BY-SA 4.0")